Scope of Assets Support Logistics.

Planning, scheduling and performance measurement are key for Logistics to achieve its Availability objective. The core of the objective is the ‘time-related positioning of internal and external resources’. These resources include people, IT applications, facilities, equipment and utilities. Organisations measure aspects of delivery for goods, but few measure the performance of internal resources to improve the Availability of goods and services for customers.

The previous blog discussed the measurement of DIFOTA and its elements in the provision of goods. The additional factor in providing Availability is to measure the performance of facilities, equipment and utilities. This is Assets Support Logistics, concerned with the overall design and operations of facilities and equipment (the system) to provide support for meeting the required level of Availability.

Assets Support Logistics relates to both the design characteristics and maintenance capability (maintenance facilities, tools and competent people) for each facility and each piece of ‘not easily moved’ equipment. The capabilities include compatibility and interchangeability, accessibility; adherence to standards and diagnostic capability.

The Logistics focus is therefore on the ‘Supportability’ (dependability and availability) of the facilities, equipment and component items that are part of the equipment.

The goals of Assets Support Logistics are to:

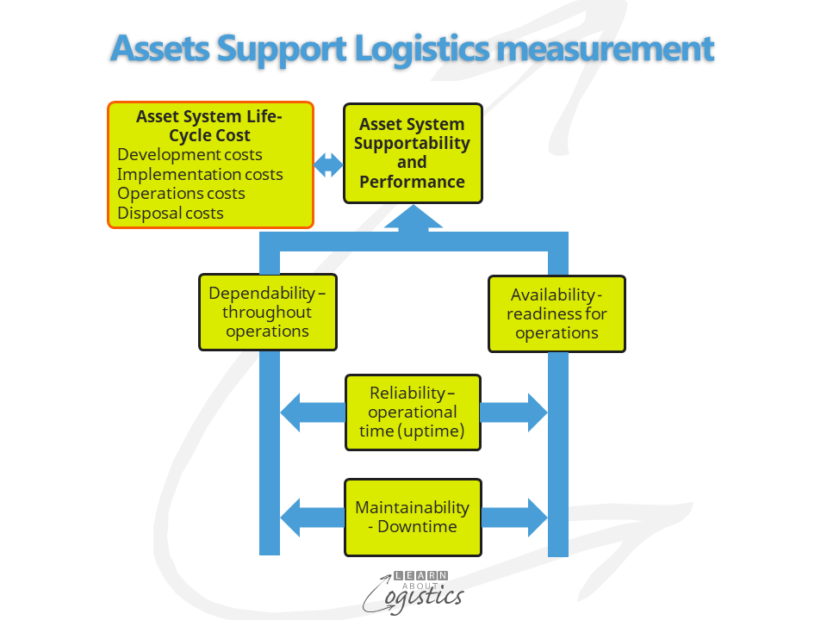

- Evaluate, with Engineering and Procurement, the consequences of design and operational decisions on the Support capability of facilities and equipment, including critical parts and components. Support capability is based on system parameters – what the unit is designed to achieve, under specific conditions. The diagram illustrates that performance is measured against the parameters and incorporates:

- Dependability: measure of the unit’s operating capability at points through an operation plan

- Availability: measure of the unit’s operable state at the commencement of an operation plan – this can be called ‘operational readiness’

- Reliability: “the probability (based on historical analysis of data, such as mean-time between failure (MTBF)) that a unit will perform in a satisfactory manner, for a given period of time, when used under specific operating conditions and that maintenance is not required more than x times in a given period” adapted from Blanchard B. Logistics Engineering and Management. Prentice Hall 1998

- Maintainability: the probability that:

- following breakdown, a unit can be restored to a specific condition within a given period of time

- a unit can be maintained, which incorporates: maintenance frequency, maintenance times (operational running time, units produced etc.) and maintenance cost

- Develop and implement the Assets Support plan

- Establish requirements for replacement and rotable parts (both on-call and held in inventory)

- Plan the maintenance requirements that cover the life cycle of the facilities and main equipment (scheduling is within the maintenance group)

- Inventory management (policy, planning and control) of items for maintenance, repair and overhaul (MRO) items

- Identify and reduce lead times and total landed cost of critical parts

- Build collaboration with the groups responsible for operations planning, procurement, accounting and IT systems

Each of these goals can be performed internally by the enterprise, tasks contracted out or complete functions outsourced to external specialist service providers. The more specific the capital equipment, the more likely that support is provided by services providers. The business priorities will reflect the organisation structure, but it does not matter whether Assets Support Logistics is located within the Engineering, Operations Planning or Logistics functions; however, planning the Assets Support life-cycle should not be outsourced.

Life-Cycle Cost (LCC)

Linked to the performance measurement of assets, the LCC approach tracks the total cost (both recurring and non-recurring) over the life cycle of an item, as noted in the diagram. The objective is to minimise total lifetime costs through considering the: performance required and associated level of support, availability of critical resources, risks and trade-offs.

Design decisions and actual operational expenditure can be at widely spaced intervals, so the LCC approach is used to link decisions and future expenditures, because support decisions, once made, can be difficult and costly to change. Estimate commonly quoted are:

- About 50% of the support decisions should be made during the facility/equipment concept, design and development stage

- After the design and development stage, only about 20% of support decisions can be changed without considerable effort and cost

- When the capital item is operational, only about 5% of support decisions can be changed without considerable effort and cost

This requires Logistics involvement in management of the processes and to minimise the LCC, requires the active input of Supply Chain professionals. One example was a company with a policy of running its capital equipment on multiple shifts for about five to eight years and then disposing and buying new.

The rationale was that capital equipment did not require heavy maintenance within the operational time period and that if disposal and purchase was timed to be in the ‘down period’ of an economic cycle, then purchase prices could be effectively negotiated. Also, warranties were negotiated out of the contract for an 8 – 13 percent price reduction. This was because the company exceeded recommended operating parameters for equipment and therefore voided the warranty.

Another example is that of co-operation among competitors located within about a 100km radius. The approach was to stock common (and expensive) imported equipment sub-assembly, components and parts at only one location (with locations spread among the companies). The stock levels were calculated, incorporating the risk of multiple demands within the delivery lead time. This reduced inventory holding costs for the businesses. When a part was used, the company placed a replacement purchase order using their billing address but the part location was the delivery address.

So, in these businesses, managing the total life-cycle costs of capital items was an integral part of corporate policy. But, to achieve this required the measurement of performance for operating assets to improve Availability of items for customers. How developed is the Assets Support Logistics concept implemented in your business?